If you are a high-earning professional over the age of 50, you are likely used to a specific year-end ritual: maxing out your 401(k) and utilizing catch-up contributions to slash your current-year taxable income.

However, a major provision of the SECURE 2.0 Act has officially gone into effect. If you cross a certain income threshold, the IRS is fundamentally changing how you are allowed to save for retirement.

Failing to adapt to this change won’t just complicate your corporate payroll—it could trigger unexpected spikes in your annual tax bill and disrupt your multi-year tax diversification strategy. Here is exactly what is happening in 2026 and how to pivot.

The New Reality: Pre-Tax Catch-Ups Are Gone for High Earners

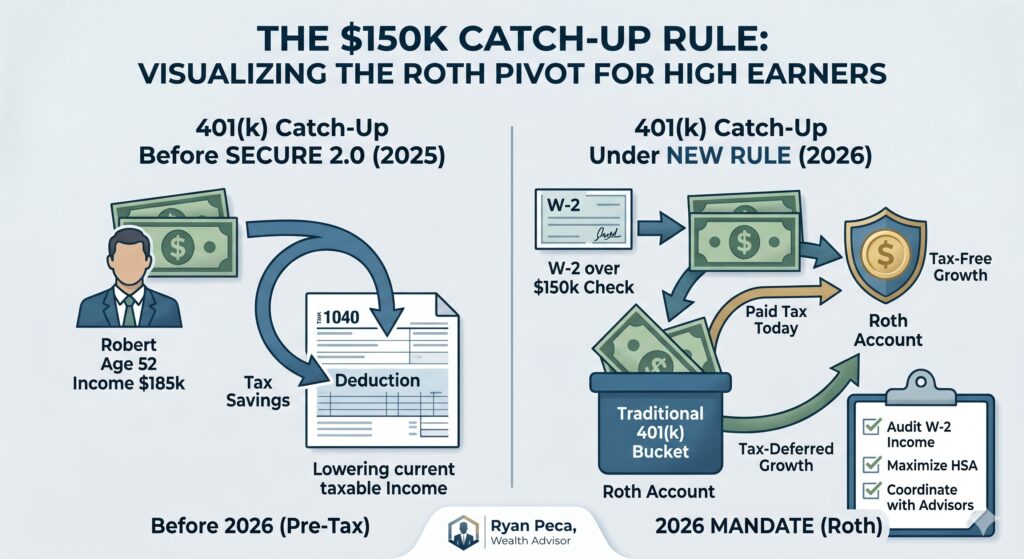

Historically, anyone age 50 or older could make an additional “catch-up” contribution to their 401(k) on a pre-tax basis.

The mandate states that if your prior-year FICA wages (Box 3 on your W-2) exceeded $150,000, any catch-up contributions you make to an employer-sponsored plan must be made on an after-tax Roth basis.

Note on the Threshold: While the initial text of SECURE 2.0 referenced a $145,000 baseline, recent IRS cost-of-living adjustments have officially indexed this threshold to $150,000 for the 2026 contribution year based on your 2025 earnings.

If you hit that $150,000 mark last year, you can no longer use your catch-up contributions to reduce your current-year adjusted gross income (AGI). Instead, those dollars will flow into a Roth 401(k). While that means you pay tax on that money today, it will grow entirely tax-free and can be withdrawn tax-free in retirement.

Knowing Your Numbers: 2026 Contribution Limits

To optimize your strategy, you first need to look at the updated limits issued by the IRS for the year.

Contribution Type | Age Bracket | 2026 Maximum Limit | Tax Treatment (Income Over $150k) |

Standard Deferral | Under Age 50 | $24,500 | Pre-Tax or Roth (Your Choice) |

Standard + Catch-Up | Ages 50 to 59 | $32,500 | $24,500 Choice / $8,000 Mandatory Roth |

Standard + Super Catch-Up | Ages 60 to 63 | $35,750 | $24,500 Choice / $11,250 Mandatory Roth |

For corporate executives and professionals in their early 60s, SECURE 2.0 does offer a silver lining: the “Super Catch-Up.” If you are between ages 60 and 63, your catch-up limit jumps to $11,250. However, if your income is over the $150,000 threshold, that entire $11,250 tier must be designated as Roth.

The Hidden Risk: Does Your Company’s Plan Support This?

This is where the rule can disrupt your planning. By law, if a company’s 401(k) plan does not explicitly offer a Roth contribution feature, no high earners in that company are allowed to make catch-up contributions at all.

While major recordkeepers have spent the last year updating their software, many corporate payroll systems are still experiencing operational friction trying to track who crossed the $150,000 W-2 threshold in the prior year.

If your company hasn’t updated its plan documents or automated this tracking, your catch-up contributions could be frozen, or worse, misclassified as pre-tax—resulting in automated payroll corrections and forced, taxable distributions back to you.

Strategic Pivots to Make with a Fiduciary Guide

A forced move into a Roth account isn’t necessarily a bad thing; tax diversification is a cornerstone of a resilient retirement plan. However, because you are losing a chunk of your current-year tax deduction, you need to proactively adjust the rest of your financial footprint.

- Rebalance Your “Tax Buckets”: If your 401(k) catch-up dollars are now forced into a tax-free Roth bucket, it may make sense to keep your base $24,500 contribution strictly pre-tax to keep your current tax bracket under control.

- Maximize Your Health Savings Account (HSA): If you have access to a high-deductible health plan, maxing out your HSA is the single best way to reclaim lost pre-tax space. It is the only vehicle that offers a “triple tax advantage”—pre-tax contributions, tax-free growth, and tax-free distributions for medical expenses.

- Examine Backdoor Roth Strategies: Because your payroll will automatically divert your catch-up space into a Roth 401(k), it is an ideal time to evaluate whether a Backdoor Roth IRA or a Mega Backdoor Roth strategy coordinates cleanly with your overall cash flow.

Align Your Plan for the Road Ahead

The new Roth catch-up mandate is a prime example of how quickly the wealth management landscape changes. What worked for your retirement blueprint two years ago might be costing you unnecessary tax friction today.

Navigating corporate payroll integration, executing advanced tax-loss harvesting, and restructuring your savings vehicles requires a comprehensive, forward-looking view.

Are your retirement accounts optimized for the 2026 rules? Placing your savings into the right buckets can mean the difference of tens of thousands of dollars over the course of your retirement. Let’s look at your current corporate benefits package together and build a tax-efficient plan. Click here to schedule a brief introductory strategy session.

Global View Capital Management (GVCM) is an affiliate of Global View Capital Advisors (GVCA). GVCM is a SEC Registered Investment Advisory firm headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262.650.1030. Registration as an Investment Advisor does not imply a certain level of skill or training. Ryan Peca is an Investment Adviser Representative (“Adviser”) with GVCM. Additional information can be found at www.adviserinfo.sec.gov Global View Capital Insurance Services (GVCI) is an affiliate of Global View Capital Advisors (GVCA). GVCI services offered through Experior Financial Group, ASH Brokerage, and/or PKS Financial. GVCI is headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262-650-1030. Ryan Peca is an Insurance Agent of GVCI.

These views do not necessarily represent the views of GVCM or any of its affiliates. Investment involves risk. The company profile is for informational purposes only and its contents should not be construed as a recommendation. The information on this social media site alone cannot and should not be used in making investment decisions. Investors should carefully consider the investment objectives, risks, charges and expenses associated with any investment.