BEYOND THE K-12 HACK: Advanced Coordination Strategies for 529s and the New 530A Accounts

Introduction: Raising the Bar on Generational Funding For years, affluent families have used "the K-12 private school hack"—utilizing a 529 plan to pay for upRead More »

The Multi-Generational 529: How to Build a Tax-Free Education Dynasty for Your Grandchildren

When most people think of a 529 plan, they picture a straightforward, single-generation tool: parents saving money so their children can afford college.But for affluentRead More »

The Three-Year Countdown: Tax Strategies You Must Implement Before the Tax Caps Snap Shut

When the historic 2017 Tax Cuts and Jobs Act (TCJA) was passed, high earners circled the end of 2025 on their calendars. It was supposedRead More »

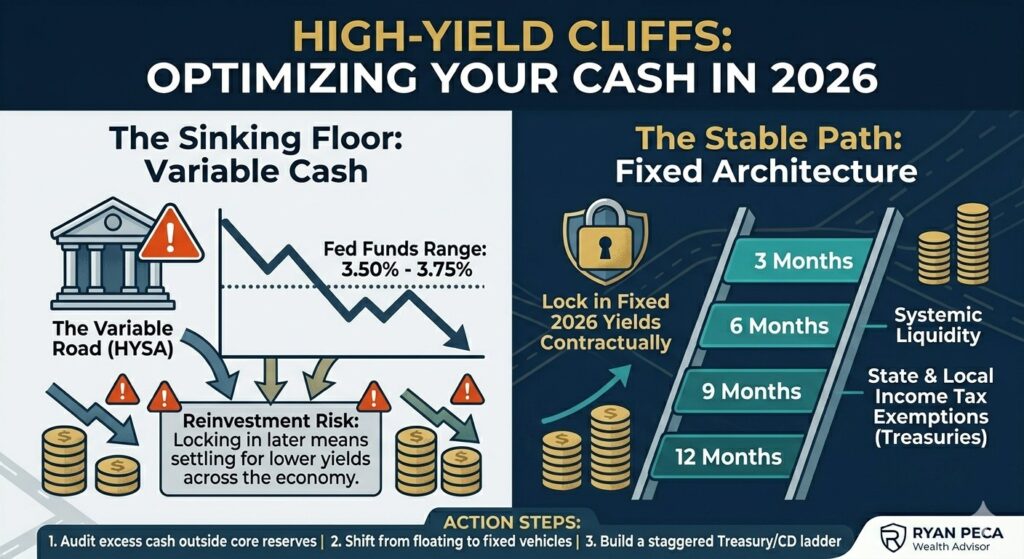

High-Yield Cliffs: Where to Reallocate Cash as Short-Term Rates Begin to Drop

For the past couple of years, cash was king, and it was entirely comfortable sitting on the throne. Following the aggressive Federal Reserve rate hikesRead More »

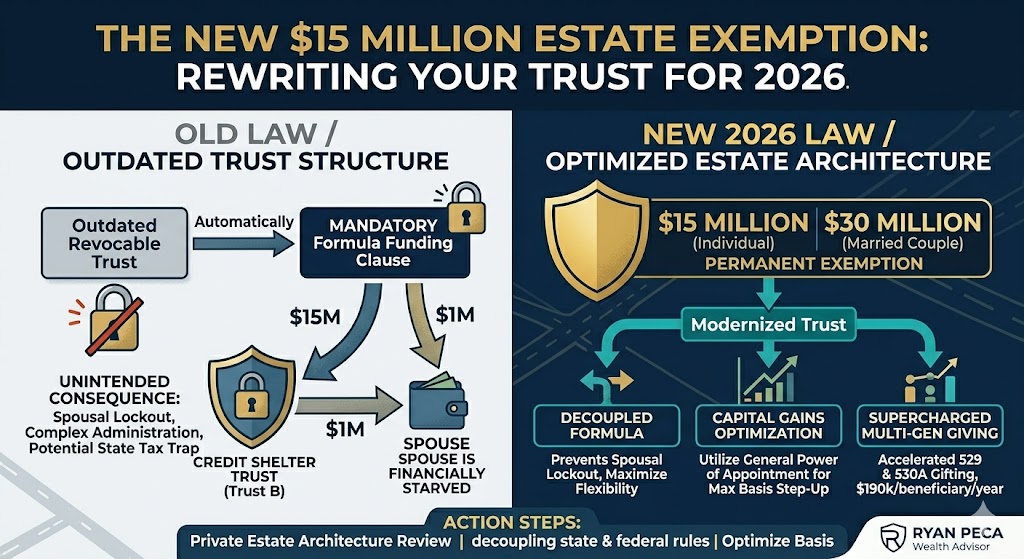

The New $15 Million Estate Exemption: Why You Must Rewrite Your Trust Under the New 2026 Law

For the last several years, high-net-worth families and business owners lived under a ticking clock. The historically high estate tax exemptions introduced by the 2017Read More »

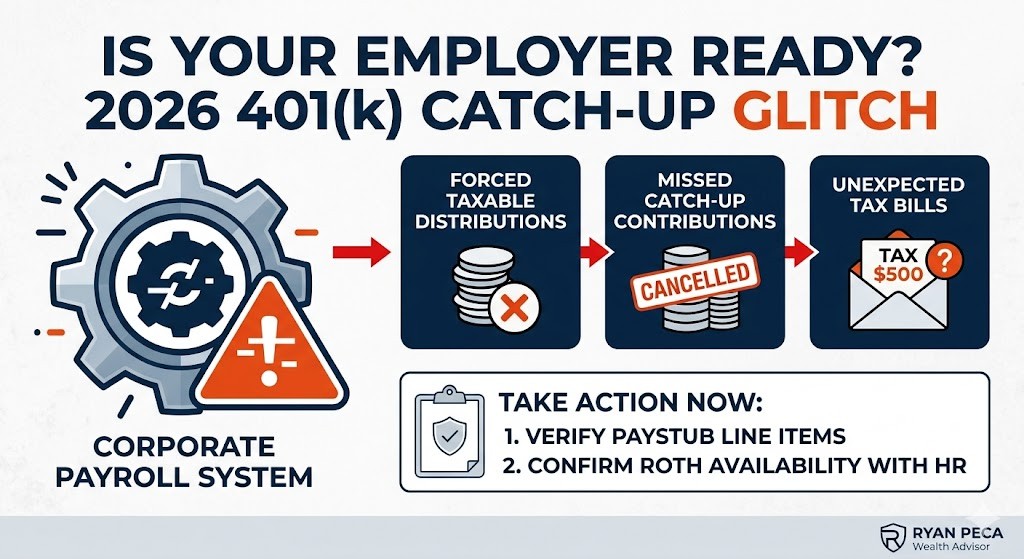

The 401(k) Catch-Up Glitch: Is Your Employer Ready for 2026?

Is Your Employer Ready? The Hidden 401(k) Catch-Up Glitch Threatening High Earners This YearThe transition to the new 2026 tax rules has felt seamless forRead More »

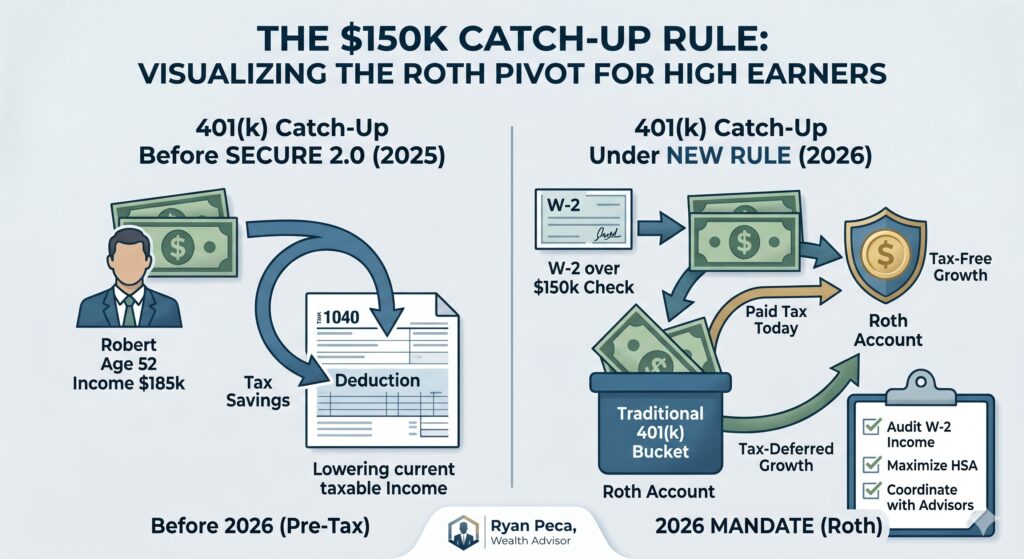

The $150K Catch-Up Rule: 401(k) Changes for High Earners (2026)

If you are a high-earning professional over the age of 50, you are likely used to a specific year-end ritual: maxing out your 401(k) andRead More »

Beyond Tuition: Using 529s for CPA Exams, Pilot Licenses, and Trade Skills

For years, the 529 plan was seen as the "University Bucket." If your child didn't want a four-year degree, many parents worried the money wouldRead More »

No More “Trapped” 529 Funds: The 2026 Guide to Roth IRA Rollovers

One of the most common hesitations I hear from parents in the Chicago suburbs is the "What If" fear: "What if I save too muchRead More »

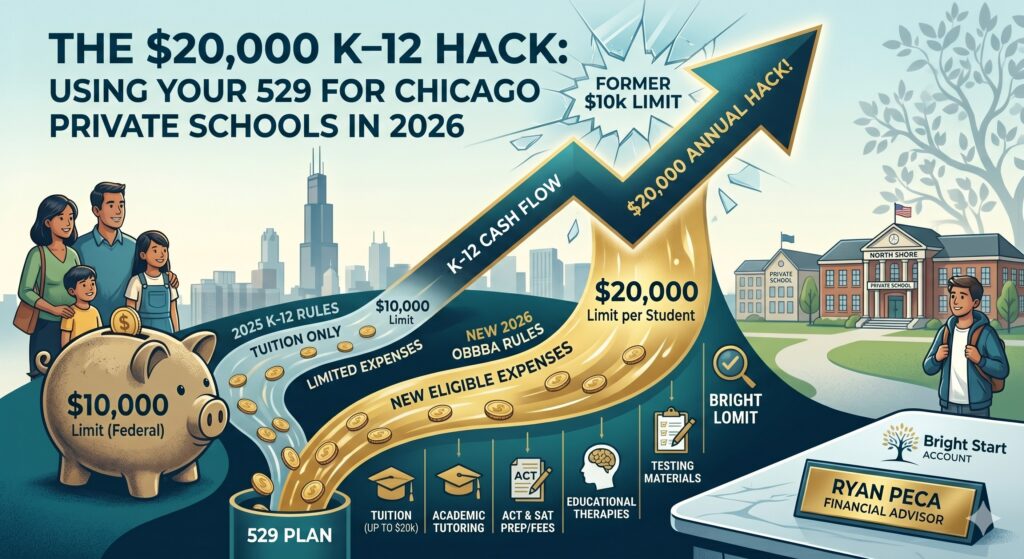

The $20,000 K–12 Hack: Using Your 529 for Chicago Private Schools in 2026

In Chicago, where elite private school tuition can easily exceed the cost of a state university, the tax-efficiency of your savings strategy is paramount. AsRead More »

529 vs. Trump Account: Which “Tax-Free” Bucket Should You Fill First?

As a fiduciary financial advisor, the question I am asked most often this quarter is: "Where should I put the next dollar for my child'sRead More »

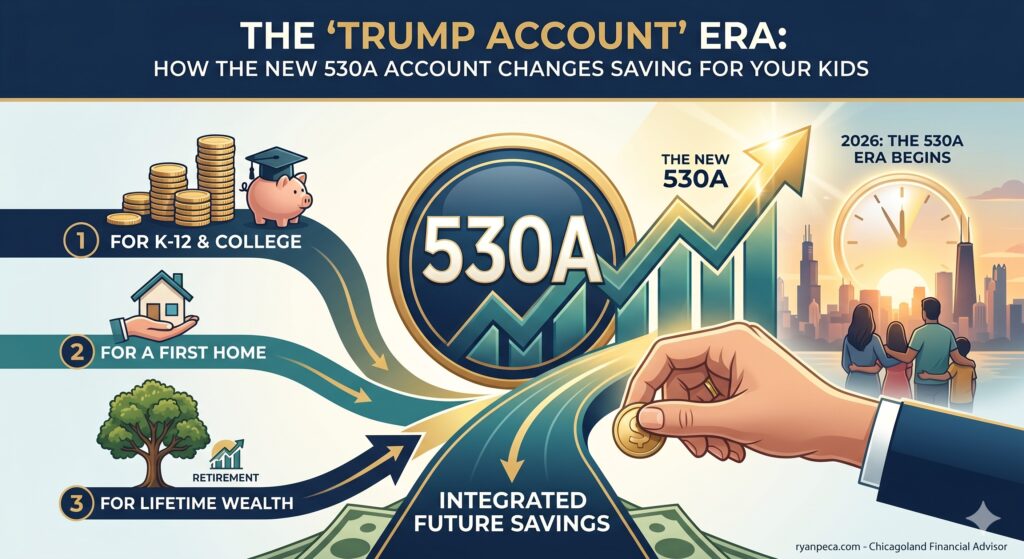

The “Trump Account” Era: How the New 530A Account Changes Saving for Your Kids

For decades, the "gold standard" for saving for a child’s future was the 529 plan. But as we move into the second half of 2026,Read More »

The 2026 Guide to Social Security: Should You Claim at 62, 67, or 70?

One of the most important financial decisions you’ll make in retirement isn’t about investments — it’s about when to claim Social Security.The difference between claimingRead More »

The “Stealth” Retirement Account: Maximizing Your HSA for Long-Term Growth

When most people think about retirement accounts, they think of 401(k)s and IRAs.But there’s a lesser-known, highly powerful tool that many investors overlook: the HealthRead More »

Where to Park Your Cash in 2026: High-Yield Savings, CDs, or Bonds?

In 2026, cash is no longer just "idle money." With shifting interest rates, inflation pressure, and market uncertainty, how you store and deploy your cashRead More »