In Chicago, where elite private school tuition can easily exceed the cost of a state university, the tax-efficiency of your savings strategy is paramount. As of 2026, a massive shift in federal law has created what I call the “$20,000 K–12 Hack.”

If you are a North Shore or Western Suburb family navigating the costs of Latin, Ignatius, or Parker, here is how the new rules—specifically the One Big Beautiful Bill Act (OBBBA)—have redefined the 529 plan from a “college-only” tool into a powerful K–12 cash-flow machine.

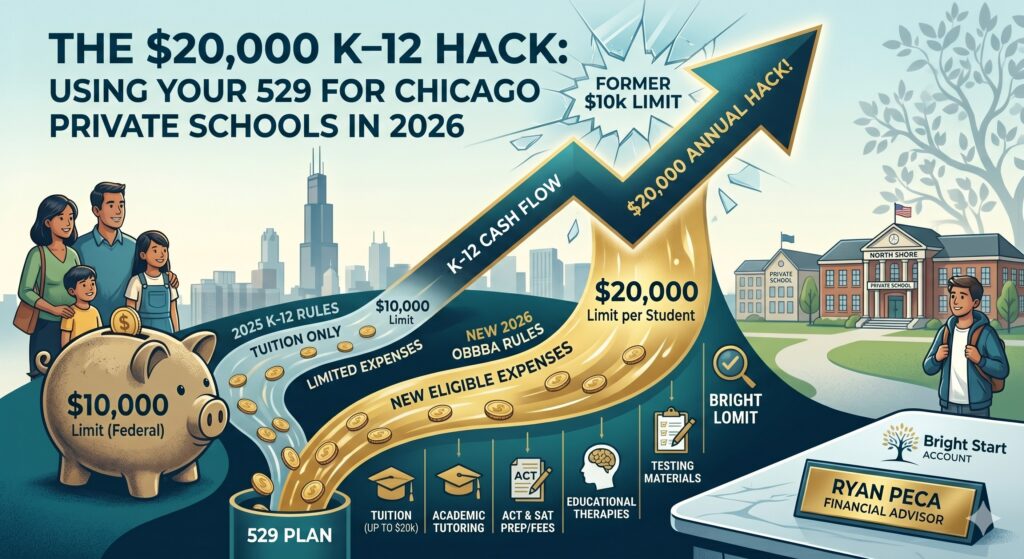

The New Math: $10,000 vs. $20,000

For years, families were limited to withdrawing just $10,000 per year from a 529 plan for K–12 tuition. In many Chicago private schools, that barely covered a single semester.

Effective January 1, 2026, the annual withdrawal limit for K–12 expenses has doubled to $20,000 per student.

For a family with two children in private school, this means you can now flow $40,000 of tax-advantaged money through your 529 accounts every single year. When you consider the compound growth and the tax savings, this “hack” can save a high-income household thousands of dollars in “real” costs over a child’s primary education.

Beyond Tuition: The “Extra” Qualified Expenses

The OBBBA didn’t just raise the limit; it expanded the definition of what you can actually buy. Historically, K–12 529 withdrawals were restricted strictly to tuition. Starting in 2026, you can now use those tax-free dollars for:

- Academic Tutoring: Vital for competitive Chicago students.

- Standardized Testing Fees: AP exams, ACT, and SAT prep.

- Educational Therapies: Critical support for students with diagnosed learning differences (ADHD, dyslexia, etc.).

- Instructional Materials: Books and curriculum for homeschooling or supplemental learning.

The Illinois State Tax Play

While the federal government has opened the doors, Illinois taxpayers have a unique advantage. In 2026, Illinois allows a state tax deduction for contributions to Bright Start or Bright Directions of up to:

- $10,000 for individual filers.

- $20,000 for married couples filing jointly.

The Strategy: Even if you didn’t start a 529 years ago, you can “pass-through” your tuition money. By contributing to an Illinois 529 and then immediately withdrawing it to pay the school (subject to the $20k federal cap), you effectively lower your Illinois taxable income by $20,000. In a state with a flat tax around 4.95%, that is nearly $1,000 in immediate cash savings just for moving money through the right bucket.

The “Superfunding” Maneuver

For grandparents or high-earning parents, 2026 offers a “Superfunding” opportunity. You can front-load five years of gift tax exclusions into a 529 plan in a single year.

- 2026 Limit: $95,000 per person ($190,000 for a couple).

- The Benefit: By putting nearly $200k into the market at once, you maximize the “time in the market” for that money to grow tax-free, even while you peel off $20,000 a year for current tuition.

Advisor Insight: Don’t Forget the “Roth Exit”

One of the biggest fears of “overfunding” a 529 for K–12 is having money left over. Remember that the SECURE 2.0 rules still apply in 2026: if your student gets a scholarship or has leftover funds, you can roll up to $35,000 of that 529 money into a Roth IRA for the child (subject to account age and annual limit requirements).

Is your 529 strategy keeping up with the 2026 laws? If you’re a Chicagoland family looking to optimize your private school cash flow, let’s look at your Bright Start accounts together. You can reach out directly at www.ryanpeca.com.

Global View Capital Management (GVCM) is an affiliate of Global View Capital Advisors (GVCA). GVCM is a SEC Registered Investment Advisory firm headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262.650.1030. Registration as an Investment Advisor does not imply a certain level of skill or training. Ryan Peca is an Investment Adviser Representative (“Adviser”) with GVCM. Additional information can be found at www.adviserinfo.sec.gov Global View Capital Insurance Services (GVCI) is an affiliate of Global View Capital Advisors (GVCA). GVCI services offered through Experior Financial Group, ASH Brokerage, and/or PKS Financial. GVCI is headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262-650-1030. Ryan Peca is an Insurance Agent of GVCI.

These views do not necessarily represent the views of GVCM or any of its affiliates. Investment involves risk. The company profile is for informational purposes only and its contents should not be construed as a recommendation. The information on this social media site alone cannot and should not be used in making investment decisions. Investors should carefully consider the investment objectives, risks, charges and expenses associated with any investment.