For the last several years, high-net-worth families and business owners lived under a ticking clock. The historically high estate tax exemptions introduced by the 2017 Tax Cuts and Jobs Act (TCJA) were legally scheduled to sunset at midnight on December 31, 2025. Wealth advisors across the country spent years warning clients that their tax-free threshold was about to be cut completely in half.

Then came the legislative package known as the “One Big Beautiful Bill Act,” which completely rewrote the playbook.

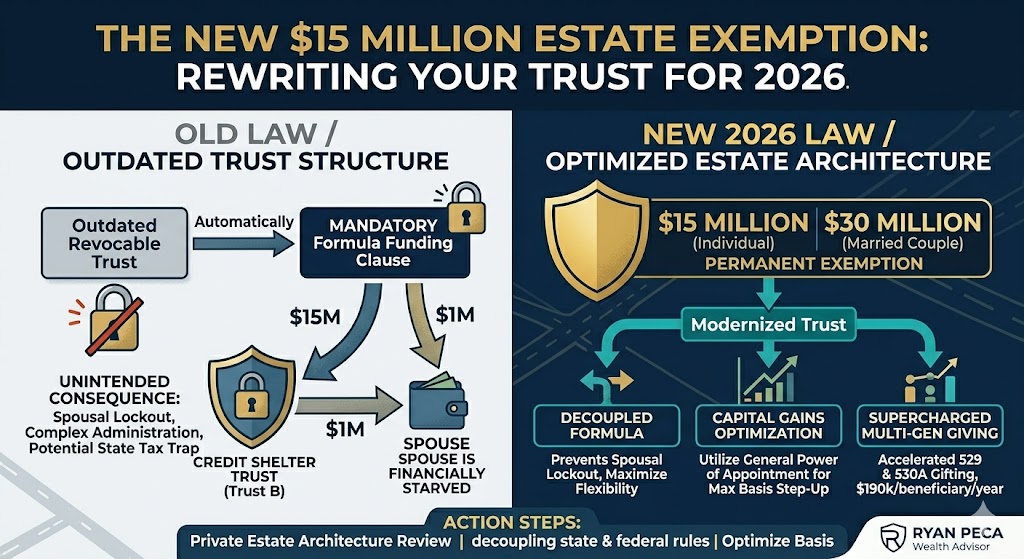

Instead of dropping down to an expected $7 million, the unified federal estate and gift tax exemption officially jumped to $15 million per individual (and a staggering $30 million for married couples) for the 2026 calendar year. Even better, this massive baseline has been made permanent and will continue to be indexed for inflation going forward.

While this is an extraordinary win for wealth preservation, it introduces a dangerous, unseen side effect: If your estate plan or trust was drafted before this year, the new law may have unintentionally broken your distribution framework. Here is why a $15 million exemption means you likely need to rewrite your trust immediately.

- The Danger of “Formula Funding” Clauses

Many revocable living trusts built for affluent families utilize what are known as “formula clauses” or “AB Trust structures.” These clauses were designed to automatically divide an estate upon the first spouse’s death to maximize tax efficiency based on whatever the federal exemption happened to be at that time.

For example, a traditional formula clause might state: “To the maximum extent possible, fund the Credit Shelter Trust (Trust B) with an amount equal to the maximum federal estate tax exemption available at my death, and place the remaining balance into the Marital Trust (Trust A) for my surviving spouse.”

Consider how this reacts under the new 2026 limits:

- The Intent: When the trust was drafted, the exemption might have been $5 million. The goal was to put $5 million into a restrictive tax-shelter trust for the kids and leave the rest directly accessible to the surviving spouse.

- The Reality Today: If an individual passes away in 2026 with a $16 million estate, the formula clause will automatically force $15 million into the restrictive Credit Shelter Trust, leaving only $1 million for the surviving spouse.

By failing to update this formula text, you could inadvertently leave your surviving spouse financially starved and legally locked out of the vast majority of your family wealth.

- State-Level “Tax Traps” Are More Severe

While the federal exemption sits at a comfortable permanent high of $15 million, many states did not follow the federal government’s lead.

States like Massachusetts, New York, and several others maintain localized estate tax exemptions that are locked at much lower thresholds—some down to $2 million or $7 million—and they do not allow “portability” between spouses.

[Federal Exemption: $15M] <—> [State Exemptions: Often $2M to $7M]

If your trust blindly ties its funding mechanisms to the federal limit of $15 million, you will accidentally trigger massive, immediate state-level estate tax bills the moment the first spouse passes away. Your trust documents must be amended to decouple state and federal planning language.

- The Shift from Estate Tax Planning to Capital Gains Optimization

With a $30 million shield protecting a married couple’s assets from the 40% federal estate tax, the vast majority of families no longer need complex, aggressive lifetime gifting strategies designed to strip assets out of their names.

Instead, the modern goal of a high-end wealth plan has pivoted to Income Tax and Capital Gains Optimization.

When assets are held inside your estate until death, they receive a “step-up in basis,” meaning your heirs can sell inherited stock, real estate, or business interests completely free of capital gains taxes based on the fair market value at your date of death.

If your current trust leaves assets inside restrictive, irrevocable wrappers meant to dodge an estate tax you no longer owe, you are forcing your children to pay massive, unnecessary capital gains taxes down the road. Rewriting your trust allows you to insert “general powers of appointment” or swap clauses that maximize the step-up in basis rules.

- Supercharging Multi-Generational Giving

The permanent $15 million lifetime limit also opens up incredible, aggressive new windows for family wealth transfers. In 2026, the annual gift tax exclusion has moved to $19,000 per recipient ($38,000 for married couples).

For families looking to clear massive blocks of wealth tax-free, parents and grandparents can now use “supercharged” five-year accelerated gifting strategies into modern 529 or 530A accounts, moving up to $190,000 per beneficiary into a tax-free compounding growth bucket in a single year without ever touching their lifetime exemption.

Take Control of Your Legacy

Legislation is never static. The permanent nature of the One Big Beautiful Bill Act gives affluent families the ultimate green light to lock in multi-generational security—but only if their documents match the current reality. Relying on a trust built for yesterday’s tax thresholds is one of the highest-risk mistakes an investor can make.

Is your estate plan optimized for the permanent $15 million rule? Let’s review your existing trust agreements alongside your current asset footprint to ensure your family is fully protected and tax-optimized under the new laws. Click here to schedule a private estate architecture review.

Global View Capital Management (GVCM) is an affiliate of Global View Capital Advisors (GVCA). GVCM is a SEC Registered Investment Advisory firm headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262.650.1030. Registration as an Investment Advisor does not imply a certain level of skill or training. Ryan Peca is an Investment Adviser Representative (“Adviser”) with GVCM. Additional information can be found at www.adviserinfo.sec.gov Global View Capital Insurance Services (GVCI) is an affiliate of Global View Capital Advisors (GVCA). GVCI services offered through Experior Financial Group, ASH Brokerage, and/or PKS Financial. GVCI is headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262-650-1030. Ryan Peca is an Insurance Agent of GVCI.

These views do not necessarily represent the views of GVCM or any of its affiliates. Investment involves risk. The company profile is for informational purposes only and its contents should not be construed as a recommendation. The information on this social media site alone cannot and should not be used in making investment decisions. Investors should carefully consider the investment objectives, risks, charges and expenses associated with any investment.