Is Your Employer Ready? The Hidden 401(k) Catch-Up Glitch Threatening High Earners This Year

The transition to the new 2026 tax rules has felt seamless for most investors on paper. However, behind the scenes of corporate America, a quiet technological storm is brewing.

As corporate executives and high earners over age 50 log into their HR portals to maximize their retirement contributions, many are running headfirst into a hidden compliance roadblock.

The mandate requiring workers with prior-year W-2 wages over $150,000 to place their catch-up contributions exclusively into a Roth account is active. But knowing the law and executing it at scale are two entirely different things—and your employer’s payroll system might not be ready.

The Core Problem: The Tracking Nightmare

For decades, payroll systems had a simple task when it came to 401(k) plans: track a single pre-tax percentage or fixed dollar amount until the employee hit the statutory annual ceiling.

The new SECURE 2.0 mandate changes everything. To remain legally compliant, your company’s payroll system must now flawlessly execute a multi-step verification process:

- Look back at the prior calendar year’s exact Box 3 FICA wages.

- Flag every single employee who crossed the $150,000 threshold.

- Automatically intercept and reroute any catch-up dollars (up to $8,000, or $11,250 for ages 60–63) into a post-tax Roth bucket, while leaving the base $24,500 contribution in the traditional pre-tax bucket.

Many legacy corporate payroll setups and mid-sized recordkeepers simply do not have automated API links that bridge prior-year tax data with real-time contribution routing.

The “All-or-Nothing” Plan Penalty

The administrative headache goes deeper than a simple software bug. Under the strict letter of the law, if an employer-sponsored 401(k) plan does not currently offer a Roth option, no high earners in that company are legally allowed to make catch-up contributions at all.

[No Roth Feature in Plan] —> [Catch-Up Contributions Banned for High Earners]

If your employer has delayed adding a Roth feature to their retirement package—or if they are experiencing delays working with their third-party administrator (TPA)—your ability to save an extra $8,000 to $11,250 this year could be frozen entirely.

How This Glitch Directly Threatens Your Wealth

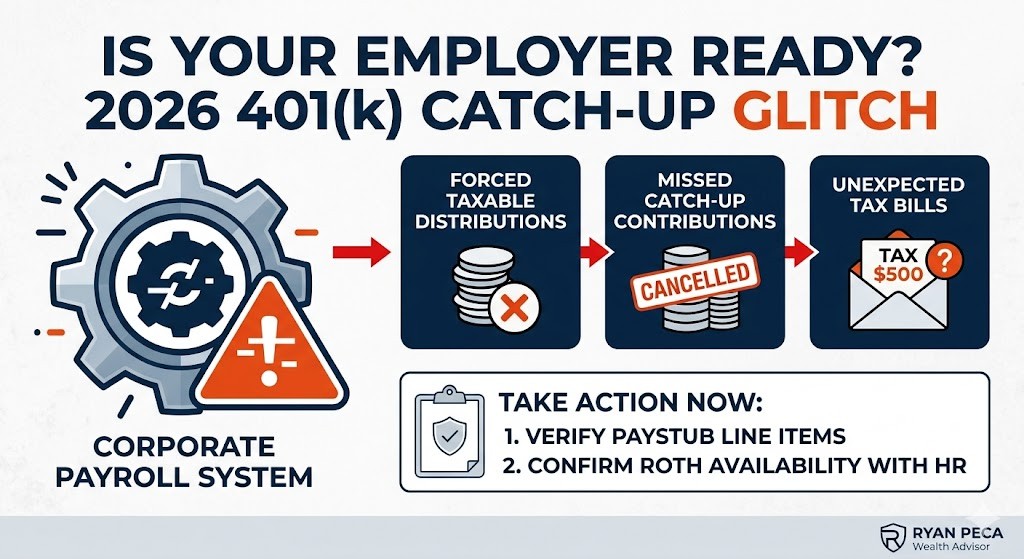

If your payroll department experiences an administrative glitch or fails to implement the proper tracking controls, the consequences fall squarely on you, the employee.

- Forced Taxable Distributions: If your system accidentally processes your catch-up contributions as pre-tax dollars, the plan will fail its annual non-discrimination testing. Your employer will be forced to issue corrective distributions—meaning that money is kicked back to you as ordinary taxable income, spiked with unexpected tax liabilities.

- Missed Market Windows: If your company hits the pause button on catch-up contributions while they patch their software, you lose out on months of compounding dollar-cost averaging in the market.

- Under-Withholding Traps: If your payroll system fails to properly calculate the immediate tax impact of shifting thousands of dollars from pre-tax to post-tax Roth, your estimated tax withholdings will be too low. You won’t find out until your CPA hands you a massive surprise bill next April.

Steps to Take with Human HR and a Fiduciary Guide

You shouldn’t wait for a corrected W-2 or a late-night email from HR to find out if your plan is compromised. Take control of your corporate benefits package with these proactive steps:

- Audit Your Paystubs Now: Look closely at your retirement line items. If you are over 50 and make more than $150,000, verify that your standard deferrals and your catch-up deferrals are listed as separate line items with distinct tax treatments.

- Ask HR the Direct Question: Send a formal query to your benefits administrator: “Has our 401(k) plan recordkeeper successfully integrated prior-year FICA lookbacks to automate the mandatory 2026 Roth catch-up provisions for high earners?”

- Coordinate Outside the Plan: If your corporate plan is facing an administrative freeze, work with a fiduciary advisor to reallocate that capital efficiently. We can pivot those dollars into maximizing an HSA, structuring a taxable brokerage account with high-efficiency tax-loss harvesting, or executing outside Backdoor Roth strategies to keep your retirement trajectory on schedule.

Protect Your Savings Infrastructure

Corporate payroll systems are built for the masses, but your financial plan requires individual precision. When systemic shifts happen, affluent professionals need a dedicated eye reviewing their total compensation packages to ensure compliance errors don’t erode long-term wealth.

Unsure if your corporate retirement accounts are processing correctly under the new laws? Let’s review your recent paystubs and benefits documentation together to ensure your plan is airtight. Click here to schedule a strategic review session today.

Global View Capital Management (GVCM) is an affiliate of Global View Capital Advisors (GVCA). GVCM is a SEC Registered Investment Advisory firm headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262.650.1030. Registration as an Investment Advisor does not imply a certain level of skill or training. Ryan Peca is an Investment Adviser Representative (“Adviser”) with GVCM. Additional information can be found at www.adviserinfo.sec.gov Global View Capital Insurance Services (GVCI) is an affiliate of Global View Capital Advisors (GVCA). GVCI services offered through Experior Financial Group, ASH Brokerage, and/or PKS Financial. GVCI is headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262-650-1030. Ryan Peca is an Insurance Agent of GVCI.

These views do not necessarily represent the views of GVCM or any of its affiliates. Investment involves risk. The company profile is for informational purposes only and its contents should not be construed as a recommendation. The information on this social media site alone cannot and should not be used in making investment decisions. Investors should carefully consider the investment objectives, risks, charges and expenses associated with any investment.