For the past couple of years, cash was king, and it was entirely comfortable sitting on the throne. Following the aggressive Federal Reserve rate hikes designed to stamp down post-pandemic inflation, savers enjoyed a historic era of 5% “lazy cash.” You could park your emergency fund, business reserves, or down payment cash in an online high-yield savings account (HYSA) or a short-term CD and watch it grow safely without taking on a shred of stock market volatility.

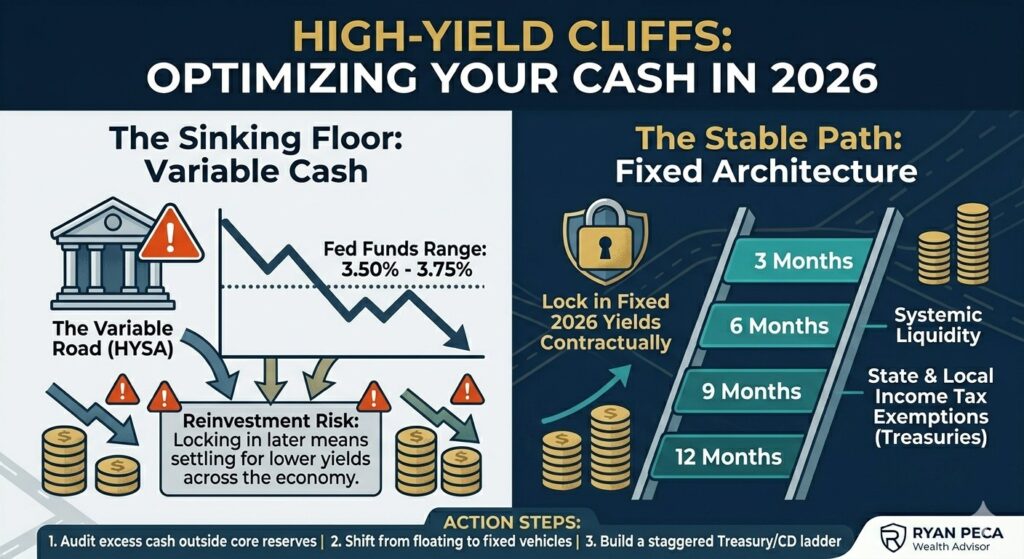

But market dynamics are shifting. The Federal Reserve has pivoted, dropping its benchmark interest rate to a target range of 3.50% to 3.75%.

As a direct result, top-tier online bank savings yields have already dropped from their 5% peaks down into the 3.8% to 4.2% neighborhood. Traditional big-box banks are offering even less. We are approaching what economists call a reinvestment cliff—and investors who leave large sums of cash floating in variable-rate accounts are about to experience a silent erosion of their purchasing power. Here is how to step off the cliff safely and reallocate your liquidity.

Understanding Reinvestment Risk: The Sinking Floor

The primary flaw of a high-yield savings account is that its rate is entirely variable. The bank can slash your yield overnight without warning to protect its profit margins as benchmark rates decline.

When you leave money in a variable account while macro interest rates drop, you are exposing yourself to heavy reinvestment risk. This means that when you eventually decide to move that money into a fixed asset later, the yields across the entire economy will be lower than they are right now.

[Fed Rate Cuts] —> [HYSA Rates Decline Automatically] —> [Lost Yield on Floating Cash]

If you are holding cash that you don’t need for immediate operational expenses or an emergency buffer, letting it sit in a declining HYSA means leaving money on the table. You need to transition from floating-rate vehicles to fixed-rate vehicles to lock in yield before the floor drops further.

The 3-Tiered Reallocation Playbook

To optimize your cash without exposing your family or business to unnecessary market risks, split your excess liquidity into three distinct strategic buckets based on when you actually need the money.

Strategy Vehicle | Time Horizon | Primary Benefit | Why It Wins Right Now |

Short-Term High-Yield | 0 to 6 Months | Maximum Liquidity | Keep your core emergency fund here to preserve transactional agility, even as rates float downward. |

Fixed-Term Certificates (CDs) | 6 to 18 Months | Guaranteed Yield | Lock in a fixed rate today. If macro rates fall further, your yield is contractually legally guaranteed for the term. |

Multi-Year Treasury Bond Ladders | 18+ Months | Tax-Advantage & Protection | Builds a staggered sequence of government-backed bonds that pay consistent income while shielding you from state taxes. |

Advanced Strategy: Constructing a 2026 Bond Ladder

For affluent families and business owners holding substantial cash reserves, a simple CD isn’t enough. The most sophisticated defense against declining rates is a custom-tailored Bond or CD Ladder.

Instead of buying one massive bond that matures all at once, you purchase a staggered sequence of high-quality fixed-income securities. For example, a standard 12-month ladder divides your cash into four equal parts:

- Tranche 1: Matures in 3 months

- Tranche 2: Matures in 6 months

- Tranche 3: Matures in 9 months

- Tranche 4: Matures in 12 months

Every three months, a portion of your wealth matures and becomes completely liquid. If you don’t need it, you simply roll it into a new 12-month bond at the top of the ladder. This creates a self-funding liquidity machine that captures high fixed yields today while giving you predictable, programmatic access to your cash four times a year.

Furthermore, by utilizing individual U.S. Treasury securities for your ladder, the interest income you earn is entirely exempt from state and local income taxes—a massive secondary win for high earners living in high-tax states.

Avoid the Cash Drag Trap

It is entirely normal to feel a sense of security when looking at a massive cash balance in your banking portal. But in a dropping-rate climate, excessive cash becomes an invisible drag on your total net worth.

Pivoting your cash management strategy isn’t about taking wild gambles in the stock market; it’s about shifting from passive saving to intentional, structural cash engineering.

Are you holding too much cash on the edge of the high-yield cliff? Let’s review your cash flow needs, analyze your emergency reserves, and construct a personalized, tax-efficient fixed-income ladder to lock in your returns before yields drop further. Click here to schedule a cash optimization strategy session.

Global View Capital Management (GVCM) is an affiliate of Global View Capital Advisors (GVCA). GVCM is a SEC Registered Investment Advisory firm headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262.650.1030. Registration as an Investment Advisor does not imply a certain level of skill or training. Ryan Peca is an Investment Adviser Representative (“Adviser”) with GVCM. Additional information can be found at www.adviserinfo.sec.gov Global View Capital Insurance Services (GVCI) is an affiliate of Global View Capital Advisors (GVCA). GVCI services offered through Experior Financial Group, ASH Brokerage, and/or PKS Financial. GVCI is headquartered at N14W23833 Stone Ridge Drive, Suite 350, Waukesha, WI 53188-1126. 262-650-1030. Ryan Peca is an Insurance Agent of GVCI.

These views do not necessarily represent the views of GVCM or any of its affiliates. Investment involves risk. The company profile is for informational purposes only and its contents should not be construed as a recommendation. The information on this social media site alone cannot and should not be used in making investment decisions. Investors should carefully consider the investment objectives, risks, charges and expenses associated with any investment.